Econbrowser: Oil market predictions: "

Oil market predictions

Cambridge Energy Research Associates seems to be substantially less optimistic than they were a year ago.

CERA received a lot of publicity last summer with their predictions of a coming glut on world oil markets. On June 21, 2005, CERA advised:

[S]upply could exceed demand by as much as 6 to 7.5 million barrels per day (mbd) later in the decade, a marked contrast to the razor-sharp balance between strong demand growth and tight supply that is currently reflected in high oil prices hovering around $60 a barrel....

If demand growth averages a relatively strong 2.2% through 2010, prices could weaken from recent record highs and slip well below $40/bbl as 2007-08 nears. If demand growth were notably weaker, a steeper price fall would be conceivable...

Global oil consumption in fact grew by a more modest 1.6% in 2005, and yet oil prices have risen since CERA made these predictions to a current value near $70 a barrel.

The Oil Drum notes that, with substantially less fanfare, CERA is now offering a much less sanguine assessment of where things are headed. The Oil and Gas Journal reports:

"Incremental additions to refining capacity over the next 2 years [will] be insufficient to meet new global demand," CERA predicts.

For the short term, CERA expects the US industry to use "innovative" methods this summer to overcome logistical hurdles involving the switch to ethanol from methyl tertiary butyl ether (MTBE) in gasoline. More than 10% of gasoline volumes in some areas are affected.

If the US Environmental Protection Agency grants waivers already authorized by the Bush administration for deliveries of nonreformulated gasoline to shortage-prone areas, supplies could be increased through imports as well.

CERA says it also expects US refiners to ramp up to full production as maintenance programs are complete and hurricane-damaged refineries come back on stream.

Nevertheless, such measures may not be enough to lower gasoline prices significantly this summer, CERA says, because of the "continued susceptibility of crude oil prices to geopolitically upward pressure" and because refining capacity additions will lag incremental demand growth, causing global refining tightness. CERA analysts expect global markets to remain tight "with exposure to potentially sharp price upswings-- even in response to small, unexpected disruptions in refinery operations."

Source: Jay Saunders, EIA 2005 Midterm Energy Outlook

|

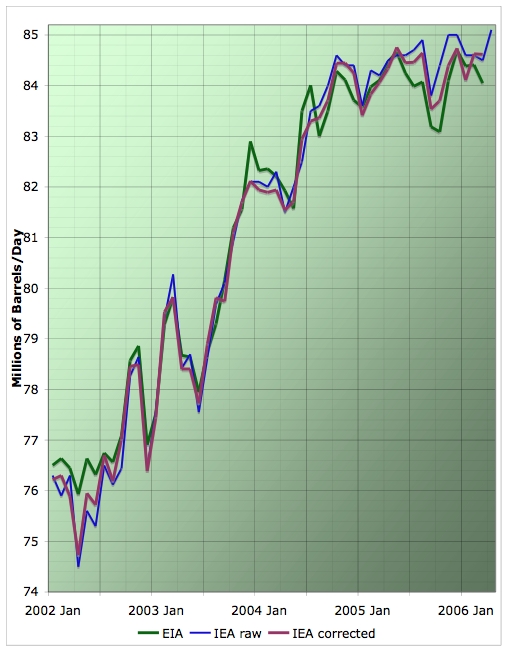

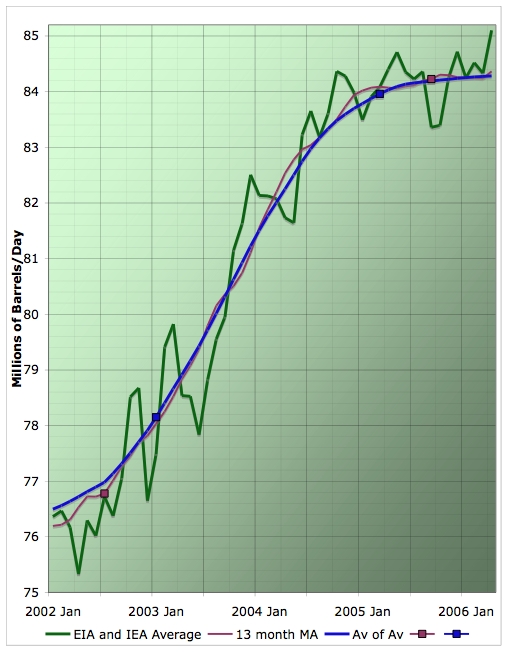

CERA's new-found pessimism in part recognizes the interaction between refining capabilities and the deteriorating quality of crude that is available to increase global production. On this theme, I have been wondering what accounts for the 400,000 barrel a day drop in Saudi production that apparently occurred in April and May, and came across this explanation from Reuters for at least part of the answer:

China will extend a 50,000 barrel per day (bpd) cut in Saudi crude oil imports into July and August after some refiners struggled to cope with new higher-sulphur supplies, industry officials said.

China contracted to buy 500,000 bpd of Saudi crude in 2006, but cut that back by 10 percent in the second quarter after refiners ill-equipped to handle the kingdom's mainly heavy-sour oil were forced to slow production after running the grades, the officials said.

That is consistent with the conjecture that the 9.5 million barrels per day the Saudis were producing in 2005 can really only be maintained with additional investing in capacity to refine the lower-quality crude they are trying to sell.

It's also consistent with another perspective that I've been advocating for quite a while. Many have articulated a vision of "peak oil" as akin to a cliff that we suddenly wake up to find ourselves to have driven off. I instead envision it as a more gradual process in which we continually pay more for oil, trying to extract lower quality stuff from harder-to-get-at locations and with increasing geopolitical risks. When asked, "what will peak oil look like?", my answer has been, "perhaps a lot like the last two years".

Elsewhere in the news, Green Car Congress noted the release yesterday of the Energy Information Administration's new report on long-term energy prospects. The EIA's benchmark forecast calls for global petroleum consumption to grow by 1.4% per year through 2030.

And where's all that new oil supposed to come from? EIA is counting on Saudi Arabia, for example, to increase its capacity to 14.4 mbd by 2010 and 17.1 mbd by 2030.

I wonder if that's another forecast that we'll see get revised."